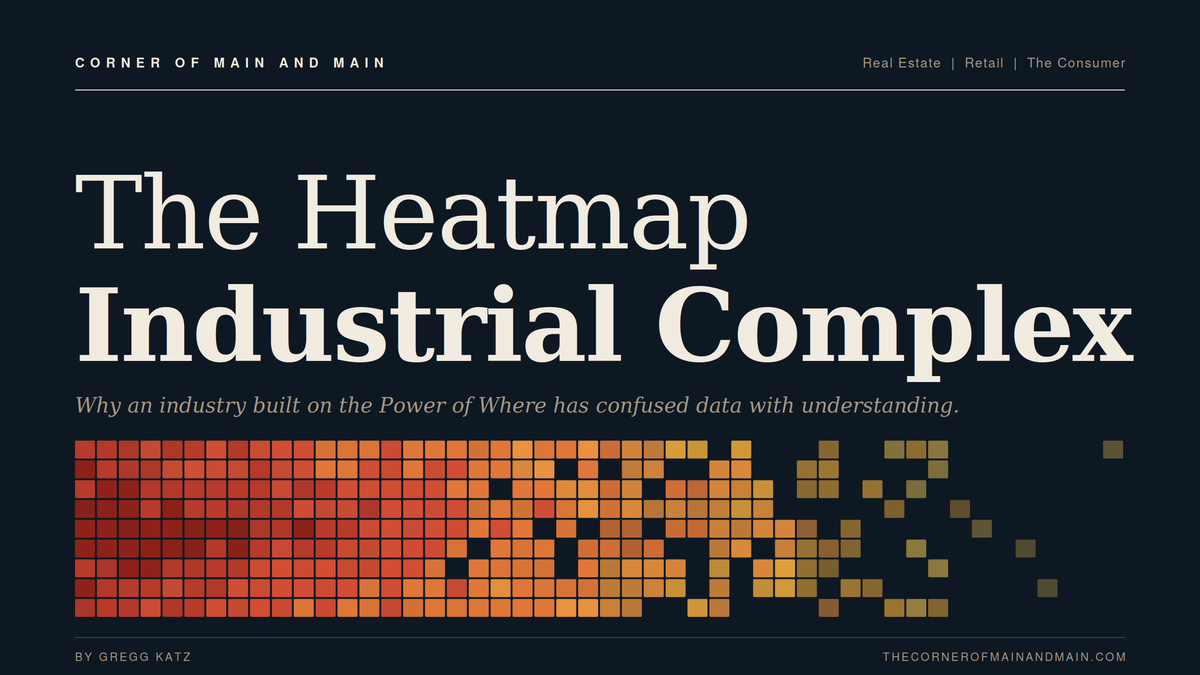

The Heatmap Industrial Complex

Why an industry built on the Power of Where has confused data with understanding, and what it costs the people making real decisions.

Walk into any commercial real estate strategy session, retail planning meeting, or lender review. You will see a heatmap.

It will be beautiful. It pulses with reds and oranges across familiar geographies. Someone will say "the data tells a clear story." Heads will nod. The deck will be saved to OneDrive and circulated on Teams. And the decision that gets made will be the one the senior leader already had in mind before the meeting started.

This is not a story about bad maps. It is a story about how an industry built on the most important question in commerce, Where, has slowly traded understanding for output.

We treat numbers as a shortcut to understanding.

That is the failure mode. And it is everywhere.

Noise wearing the costume of logic

In today's information-rich environment, logic has become noise. Clients are inundated with specs, facts, and claims. Every vendor delivers more layers, more variables, more visualizations, more dashboards. The volume of analysis goes up. The quality of decisions does not.

The result is a strange paradox. The more data we produce about a place, the less anyone seems to understand it.

A heatmap of foot traffic does not tell you whether to open a store. A shaded map of household income does not tell you which trade area to enter. A bubble map of competitors does not tell you where to locate. These artifacts describe the world. They do not interrogate it. And the gap between describing and interrogating is where most location work goes to die.

We have mistaken the production of data for the practice of understanding. We have mistaken dashboards for decisions. We have mistaken volume for insight.

The Power of Where is real

Place matters. Where matters.

The discipline of location intelligence is foundational to retail, real estate, logistics, finance, and most other industries that touch the physical world. The geography of where customers live, where competitors operate, where infrastructure exists, where regulation applies, and where talent gathers shapes nearly every commercial outcome that matters.

The Power of Where is not the problem. The problem is that this power has been diluted by an industry-wide habit of producing more outputs and less meaning. We have made it easy to generate a hundred maps and hard to generate one defensible recommendation. We have made beautiful what should be useful and abundant what should be precise.

The discipline is real. The deliverables have become decoration.

Two kinds of work

There are two kinds of location work, and we should stop pretending they are the same.

The first is decorative. It exists to make decisions feel grounded. To put a logo, a map, and a number on a slide. To justify what was going to happen anyway. Decorative work is the appendix in a real estate committee memo. It is the quarterly market review nobody reads twice. It is the executive dashboard that hasn't been updated in six weeks and nobody has noticed.

The second is consequential. It changes what gets built, where capital flows, which markets get prioritized, which stores get closed, which neighborhoods get served. Consequential work is harder. It requires asking uncomfortable questions. It requires modeling honestly. It requires being willing to deliver an answer the executive sponsor does not want.

Both produce maps. Only one produces meaning.

Why the noise wins

Three reasons the decorative dominates.

First, dashboards are easier to procure than understanding. Buyers procure platforms. Platforms produce outputs. Outputs feel like progress. The result is volume, not value.

Second, visualization is designed to please. The visual grammar of geography (boundaries, gradients, clusters) creates a sense of insight even when the analysis is thin. Aesthetic clarity gets mistaken for analytical rigor.

Third, the customer is often not the decision maker. Analytics teams produce work for executives who never open the file. The work product becomes its own justification. Maps get made because maps are what this team makes.

In every case, the answer to "what does the data mean" gets quietly replaced by "look at how much data we have."

What consequential looks like

Consequential location work has tells.

It is comfortable disagreeing with the deal sponsor. It models cannibalization before celebrating new openings. It distinguishes between markets you can win and markets you can simply enter. It quantifies what happens if you do nothing. It is willing to recommend closure, divestiture, or exit. It treats the map as a starting point, not an ending one.

It also tends to look quieter. The output is often a memo, a model, a specific recommendation tied to a specific dollar amount. The visualization, when it appears, is in service of the argument and not a substitute for it.

Consequential work earns its conclusions. Decorative work decorates them.

The honest reckoning

The Power of Where is not in question. Geography matters. Spatial reasoning is foundational. The discipline has more to offer the commercial world today than at any point in history.

But the discipline and the deliverables are not the same thing. And the industry has been hiding behind the deliverables for too long.

If you are buying location intelligence, ask harder questions. Not "what does the data show," but "what questions does it answer, what does the data recommend, and what are you willing to be wrong about." Not "can you map this," but "what decision does this map change."

If you are producing location intelligence, do less and mean more. Produce fewer dashboards and more arguments. Treat each output as a claim that has to earn its place in someone's decision.

Place is meaning. Where is meaning. The map is not the meaning. It is the invitation to find it.

The heatmap industrial complex thrives on volume. The discipline it claims to represent thrives on consequence.

It is past time we picked one.

IN THE NEWS

The great American data center divide

"Many rural communities are viscerally opposed to AI infrastructure."

AI’s Impact on Malls and Stores: The Good, Bad and the Inevitable

"By 2030, the U.S. B2C retail market could see up to $1 trillion in revenue from agentic commerce, with global projections reaching as high as $3 trillion to $5 trillion, according to McKinsey research."

CoStar: Industrial Vacancy Will Peak in Early 2027

"U.S. industrial vacancy is projected to rise into early 2027, according to a revised forecast from CoStar Group."

Lenders are finally cutting losses on troubled CRE loans.

"After years of delaying difficult decisions on troubled commercial real estate loans, lenders are finally beginning to cut losses, sell distressed debt, and foreclose on struggling properties amid intensifying pressure across the sector."

Gap closes its last Oakland store after 26 years

"A longtime apparel retailer is exiting another market as store closures reshape the future of brick-and-mortar shopping."

NOSTALGIC RETAIL SPOTLIGHT:

BUILDER'S SQUARE

A category killer that got to scale, hit $1.9B in sales, and still lost. Because nobody asked what made the category specific in the first place.

Before Home Depot owned every weekend DIYer's imagination, Builder's Square was already there.

Founded February 1970 in San Antonio as Home Centers of America by Frank Denny, a former W.R. Grace executive who saw the warehouse format coming a decade before most retailers did. Unusual for the era: the company went public from day one.

July 1984. Kmart wrote a check for $88.2 million ($225M in today's dollars) and rebranded the chain Builder's Square. Denny stayed on. The format scaled fast. 100,000 square feet. 35,000+ SKUs. Knowledgeable staff. A category killer in waiting.

By 1988, Builder's Square hit $1.9 billion in sales across 180 stores. By 1994, 184 locations in 24 states. Kmart poured in another $700 million. Tim Allen, Darrell Waltrip, and the Alamo Bowl carried the brand into living rooms across America.

The chain looked invincible. Then the math turned.

Home Depot had a deeper bench and faster expansion. Lowe's quietly converted from small-format hardware into full category warfare. Kmart, meanwhile, was fighting Walmart and bleeding cash at the core.

July 1997: Kmart sold Builder's Square to Leonard Green & Partners, who merged it with Hechinger into what was briefly the #3 home improvement chain. 279 stores. $4.5B in revenue.

It didn't matter.

June 1999: Hechinger filed Chapter 11. September 1999: liquidation. The remaining boxes flipped to Home Quarters Warehouse, then went dark.

The lesson isn't that Home Depot won. The lesson is that Builder's Square got there first, scaled to $1.9B, and still lost. Because Kmart treated a specialist category as if it were just more retail.

"Retail is retail" is how you fund a category killer's competitor with your own balance sheet.

The same shortcut that loses companies in 1999 still loses them in 2026. The shortcut of treating something specific as if it were general. Treating place as just data. Treating a category as just another box.

The mistake didn't die with Builder's Square. It's playing out right now in grocery. In pharmacy. In mass apparel. And it will keep playing out as long as the industry rewards the appearance of understanding over the practice of it.