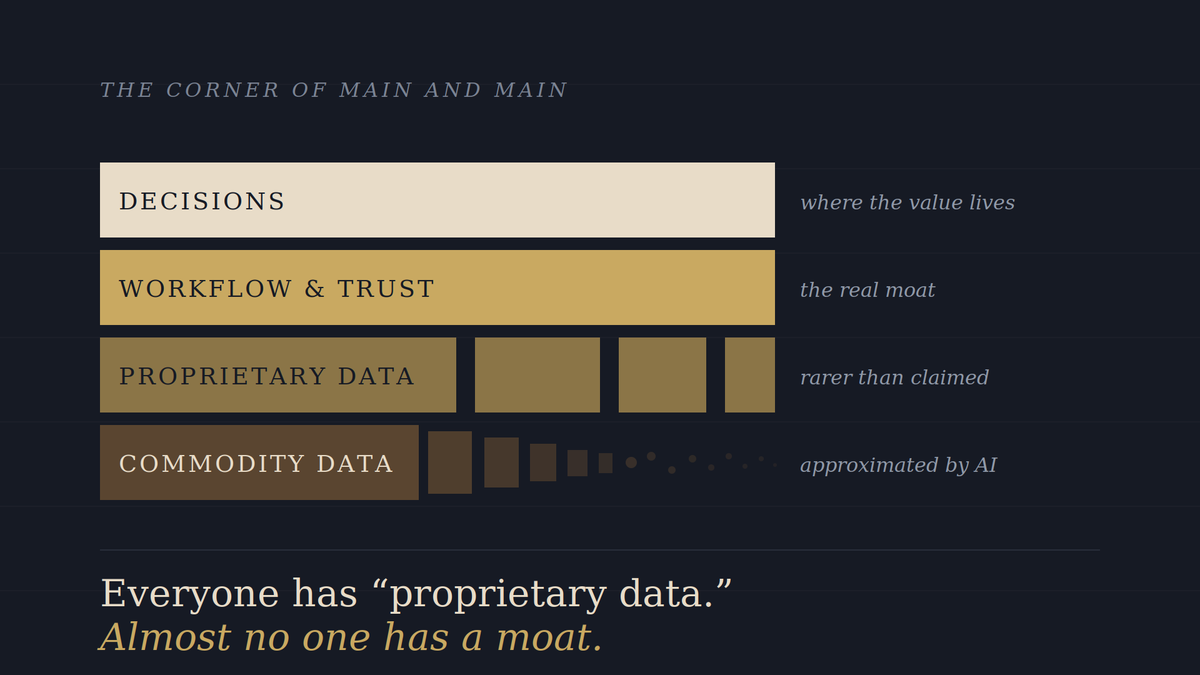

Everyone Has "Proprietary Data." Almost No One Has a Moat.

Sit through enough data vendor demos in #CRE and you start to notice something. Every dataset is "proprietary." Every platform has a "unique edge." Every company is the only one who can give you "this view of the market."

Funny thing - pull back the curtain on many of them and you'll find the same underlying sources, just weighted, packaged, and rebranded a little differently.

Proprietary has become the most overused word in the data business. And in an AI-powered world, the people leaning hardest on it are about to find out it doesn't mean what they think it means.

What Are We Actually Calling Proprietary?

Brian Lichtenberger wrote a piece recently called Proprietary Data Is Not What You Think It Is that's worth reading in full. His core argument is one most of us in this industry need to wrestle with: the word "proprietary" tends to get treated as binary. You either have it or you don't. And if you have it, it must be valuable.

That framing falls apart fast in practice.

If a competitor has data that's functionally similar but sourced from a different pipe, are you still proprietary? If your data comes from broadly available sources but you've cleaned, enriched, and embedded it into a workflow that actually drives decisions, is that proprietary?

In CRE, the line is even blurrier. Look around our space and you'll see half a dozen vendors selling some version of the same insights: overlapping visitation, overlapping demographic overlays, overlapping trade area math to roughly the same buyers. Plenty of those vendors are running real businesses with real customers. Not because the underlying data is unique to them. Because their packaging, their integration, and their customer relationships are.

Exclusivity isn't what's getting paid for. Execution is.

The Three-Bar Test

Lichtenberger pulls in a framework that's worth sitting with. For a dataset to actually function as a moat — not a marketing line, an actual moat — it has to clear three bars at the same time. It has to genuinely matter to a real decision someone is making with real money. It has to actually set you apart in a way a competitor can feel. And it can't be something a sharp team could approximate from public sources for a fraction of the cost.

Most "proprietary" datasets fail at least one. A lot of them fail two.

Plenty of datasets are unique but unimportant. Plenty are important but easy enough to approximate. Plenty are genuinely hard to replicate, but the buyer doesn't care enough to pay real money for them. The Venn diagram of all three overlapping is much smaller than the industry wants to admit.

I'd add one more layer for our world. In CRE, the real moat was rarely the dataset to begin with. It was the workflow built around it. The relationships. The judgment layered on top. The dataset is the ingredient. The moat is the recipe. And the recipe is what people are actually paying for, whether they realize it or not.

Data Is Only Worth What Someone Will Pay For It

Jonathon Schuster wrote a post recently that gets at this from the seller's side. He'd built a data product the way most people build a data product. Strong volume, a tight platform, an integration story, a pricing page. He figured the quality of the data would carry the deals.

It didn't. The pipeline stalled. The deals dragged. The phone didn't ring the way the spreadsheets said it should.

His takeaway is one every data vendor in our space needs to sit with. Nobody is opening their wallet for a dataset. They're opening it for the answer to a question that's costing them money right now, delivered inside a workflow they already live in, with someone they already trust standing behind it. If your data doesn't fit that shape, it doesn't matter how proprietary it is. You're sitting on inventory, not a business.

This is where most "proprietary data" pitches quietly collapse. The dataset is interesting in isolation. The link to a buyer's actual decision is fuzzy.

Fuzzy doesn't write checks.

The Bias Inside the Box

Here's where it gets harder. Even when data does drive a decision, the way it's framed shapes the answer.

Run the same trade area through three different platforms and you'll get three different "truths." Different boundaries. Different weighting. Different visitation models. Different conclusions about whether a site works. Same trade area. Different stories.

Data isn't neutral. Someone made choices about what to include, what to leave out, how to clean it, how to model it, how to display it. Those choices are baked into the answer before you ever ask the question.

That doesn't mean the data is wrong. It means the data has a perspective. And if you're making a multi-million dollar real estate decision based on it, you'd better know what that perspective is.

The best operators I know don't just ask, "What does the data say?" They ask, "What did the data have to assume to say that?"

That's a different muscle. It's the one that separates real insight from very expensive confirmation bias.

Then AI Walks In

Now layer AI on top of all of this.

AI is collapsing the cost of collecting, synthesizing, and approximating datasets that used to take years to build. Work that required a team of analysts can now be roughed out by an agent in an afternoon. The floor is rising. Fast.

Here's the twist: AI cuts both ways.

For commodity data dressed up as "proprietary," AI is going to be brutal. If a foundation model can approximate 80% of your value from public sources and well-framed prompts, your moat was never a moat. It was a head start. And head starts evaporate.

But for the data that actually is differentiated...the stuff generated by your own customers, your own behavior signals, your own context, the stuff that gets richer the more it's used and can't be inferred from anything public, AI does the opposite. It makes that data more valuable, not less. AI is the engine. Real proprietary data is the fuel no competitor can buy at the pump.

The bar for what counts as proprietary just got significantly higher.

What This Means for the Industry

If you're a vendor selling data into CRE, the questions to start asking:

- Are customers buying my data, or buying the workflow it lives inside?

- If a competitor showed up tomorrow with 80% of my dataset and a cleaner interface, what would actually hold my customers in place?

- Where am I building compounding advantages, and where am I just renting out rows and columns?

If you're a buyer, the principle is the same, the lens just flips:

- What decision is this data actually informing, and how would I know if it pointed me wrong?

- What perspective is baked into how it's framed, and does that perspective serve me or serve the vendor?

- What happens to my workflow if this vendor disappears, or if AI commoditizes their inputs in 18 months?

Bringing It Home

"Proprietary data" is becoming the "experiential retail" of the data world. A phrase everyone uses, few can actually define, and most are leaning on to dress up something less defensible than they want to admit.

Real proprietary data still exists. It's just rarer than all of the presentations and demos that mention it suggest. And the moat around it is shrinking by the month unless it's wrapped in workflow, trust, and a use case someone will pay for over and over again.

In an AI-powered world, owning the data isn't the win. Owning the layer where the decision actually gets made and getting to the speed of insights faster than anyone else...that's the win!

So the question isn't, "Do you have proprietary data?"

The question is: when AI can approximate 80% of it tomorrow, will anyone still be paying for what's left?

IN THE NEWS

Fast-food, fast-casual restaurants losing dining ground to convenience and grocery stores

"Report from Tillster says consumer shift is creating ‘one of the most fragmented foodservice landscapes in history’"

AI Doesn't Replace Human Judgment in Retail Real Estate - Where We Buy #375 (Video from James Cook )

"Paul Sill uses data and predictive analytics to help retailers, restaurants, and other brick-and-mortar businesses make site selection decisions. Paul explains the critical difference between correlation and causation in retail data, explaining that misreading data can lead to costly mistakes."

What Drives Office Use and Occupancies? Hint: It’s Not About Class

"Terms like “flight to quality” and “bifurcation” have been part of the office discussion since the pandemic. The belief is that tenants prefer newer, amenity-filled Class A buildings to older, Class B or C buildings."

Authentic Brands Group Is Bringing Barneys Back

"The luxury retailer will return to its original location on Madison Avenue, according to a source familiar with the matter."

Commercial mortgage delinquencies climb again

"New MBA data pointed to rising early-stage trouble across key property types"

Nostalgic Retail Spotlight: PARTY CITY

With the announcement that Party City will have a presence in Staples, I thought it might be a good idea to revisit this one as it makes a hybrid brick and mortar return!

I am currently posting a series on nostalgic retail on LinkedIn and have compiled it all on a website. Want to see what you have missed? Click HERE

Founded by Steve Mandell in 1986 in New Jersey, Party City was the largest seller of party goods (and balloons) in the United States.

His first year in business was very successful with plans made to grow, to franchise as well as the decision to focus on Halloween with 25%+ of the store space dedicated to Halloween costumes. By 2015, $560 million (or 25% of revenue) came from the 300 or so Halloween City pop-up locations.

In 1989, Party City started franchising with store count growing to 58 by the end of 1993, with revenues of over $2.4 million.

In 2005, Party City was sold to Amscan, a party good manufacturer and distributor. This led to an acquisition spree consisting of Party America in 2006 and Factory Card & Party Outlet in 2007, converting these locations to the Party City brand.

"With Amscan's 2011 acquisition of American Greetings' Designware party division, Party City added licensing agreements with Nickelodeon, Sesame Workshop, and Hasbro. In 2011, Amscan became a licensee for MLB, NBA, NFL, NHL, and NCAA party products and balloons, with Party City carrying all teams in their respective markets and offering the entire assortment in larger stores and online." [Wikipedia]

After being acquired again in 2012 and a sale of a majority stake in 2015, Party City placed itself on the market in 2017 as a response to a lot of private equity interest.

With continual struggles related to the pandemic, helium shortages, intense competition from big box retailers and consumer behaviors, Party City filed for Chapter 11 bankruptcy protection in January of 2023. The company secured financing to keep operating and completed bankruptcy reorganization in September of that same year. With no significant improvement and out of cash, December 2024 brought on a second bankruptcy filing . The company announced all stores would close by the end of February 2025.

U.S. locations not operated by the company can remain open, but the impact to the brand may be too much for these locations to continue long term which is why they have ended up in the last position on this list...they are effectively an immediate nostalgic brand.